As the need for senior care continues to grow, families are faced with many choices about how to best support their loved ones. From in-home care to assisted living and nursing homes, each long-term care option offers unique benefits and costs. Use this infographic to explore the different types of long-term care available and what to consider when planning ahead.

Share this Image On Your Site

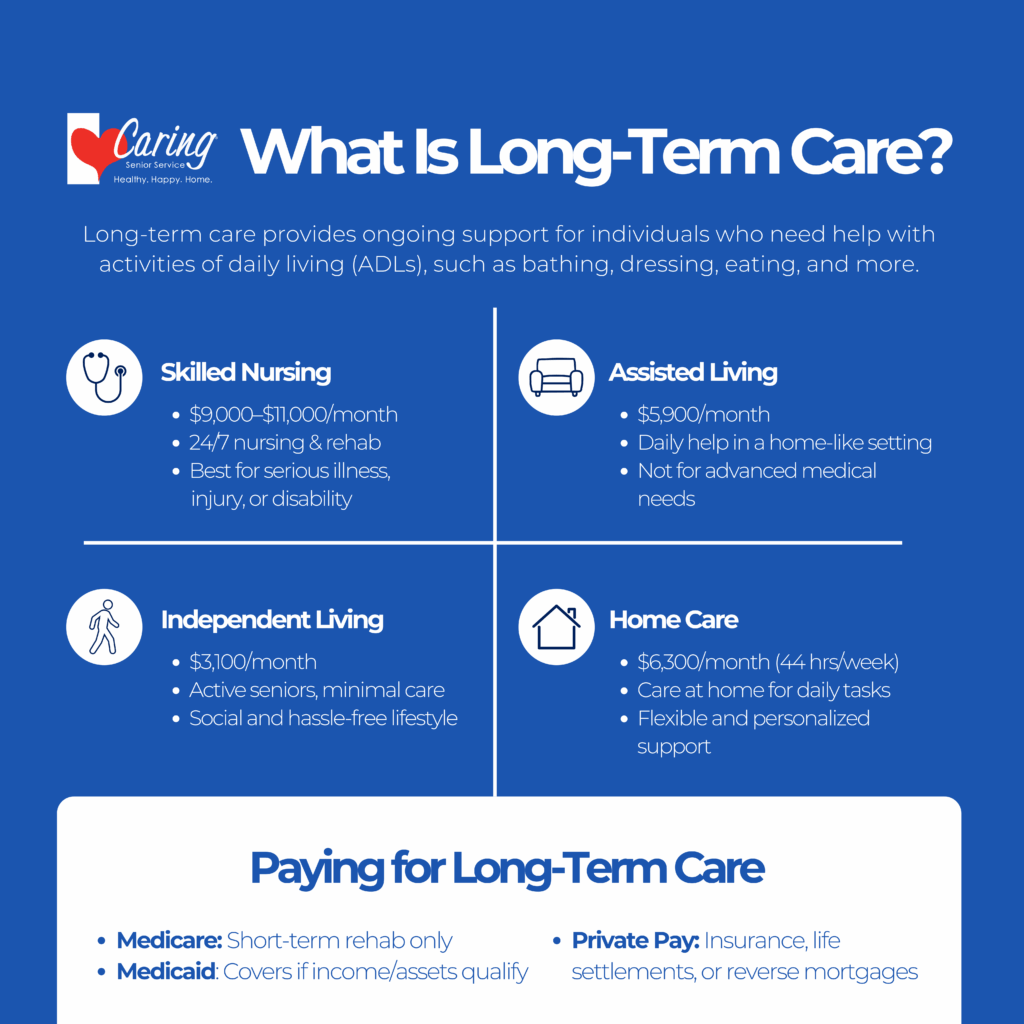

Understanding Long-Term Care: Options, Costs & Coverage

As America’s population ages, conversations about long-term care are becoming more important than ever. Long-term care (LTC) refers to the support people need when they can no longer manage daily tasks on their own due to age, illness, or disability. While many families hope these needs won’t arise, planning ahead can help reduce stress and protect both financial and emotional well-being.

In fact, nearly 70% of adults age 65 and older will need some form of long-term care during their lifetime. That makes it critical for families to understand what care looks like, how much it costs, and what options exist.

This guide walks through what long-term care means, the most common care options available, average costs across the United States, and ways families can pay for it. Dive into additional details in the content below the infographic to better understand your loved one’s future needs.

What Is Long-Term Care?

Long-term care includes a wide range of services designed to help individuals with activities of daily living (ADLs). ADLs include basic tasks like bathing, dressing, eating, and using the bathroom. Some individuals also require help with instrumental activities of daily living (IADLs) such as cooking, cleaning, shopping, or managing medications.

Contrary to popular belief, LTC is not just for older adults. A younger person with a disabling accident or chronic illness may also require long-term care. Still, seniors represent the largest group that needs these services.

At its core, long-term care focuses on maintaining safety, independence, and dignity. Whether provided in a senior living community or at home, these services help people live with as much comfort and autonomy as possible.

Types of Long-Term Care

Families today have more choices than ever when it comes to long-term care. Each option varies in cost, levels of care and medical oversight, and lifestyle benefits. Understanding the differences can help family members find the best fit for their loved ones.

Skilled Nursing Facilities

Skilled nursing facilities (often called nursing homes) provide the highest level of medical care outside of a hospital. These centers have nurses and staff on duty 24/7, along with rehabilitation services such as physical, occupational, and speech therapy.

- Best for: Individuals with serious medical conditions, advanced illness, or those recovering from major surgery or injury.

- Average cost: Median rate of $9,000–$11,000 per month (semi-private vs. private room).

Skilled nursing care can be temporary for recovery or long-term for chronic conditions that require continuous monitoring.

Assisted Living Facilities

Assisted living offers a balance of independence and support. Seniors typically live in private apartments while receiving assistance with activities of daily living, meals, housekeeping, and social programming. Many facilities also provide transportation and medication management.

- Best for: Seniors who need some assistance but do not require round-the-clock medical care.

- Average cost: Median rate of $5,900 per month.

For families, assisted living often provides peace of mind that loved ones are in a safe and social environment.

Independent Living Communities

Independent living is ideal for healthy, active seniors who want a maintenance-free lifestyle and access to social opportunities. These communities may offer meal plans, housekeeping, and recreational activities, but provide little or no personal care.

- Best for: Seniors with minimal medical needs who want to downsize or enjoy a more community-focused lifestyle.

- Average cost: Median rate of $3,100 per month.

Independent living can be a first step before transitioning into assisted living or home care if more support becomes necessary.

Non-Medical Home Care

Many families prefer to keep their loved ones at home for as long as possible. Non-medical home care provides assistance with everyday tasks in the comfort of the client’s own home. Care schedules can range from just a few hours a week to full-time.

- Best for: Seniors who want to age in place with flexible, personalized support.

- Average cost: Median rate of $6,300 per month (based on 44 hours/week of care).

Home care also provides companionship, which can be vital in reducing loneliness and social isolation.

Note: Home health care is different from home care. Home health provides short-term medical services at home, such as wound care, physical therapy, or medication management, usually after a hospital stay and prescribed by a doctor. Home care, on the other hand, focuses on non-medical support with daily living. Many families use both together to meet changing needs.

The Rising Cost of Long-Term Care

The cost of long-term care continues to climb year after year. According to the 2024 Genworth Cost of Care Survey, actual costs vary widely by state and even by city. For example, care is often more expensive in urban areas than in rural regions.

With the senior population projected to double by 2060, families can expect costs to continue rising in the coming decades.

How to Pay for Long-Term Care

Affording long-term care can be one of the biggest challenges families face. Understanding what is and isn’t covered by insurance or government programs can help you prepare.

Medicare

Many assume Medicare covers long-term care, but this is a common misconception. Medicare only pays for short-term rehabilitation after a qualifying hospital stay, not for ongoing custodial care.

However, Medicare has recently launched the GUIDE Program (Guiding an Improved Dementia Experience). This program provides care coordination, caregiver education, and respite support for individuals living with dementia and their families. While it does not cover full-time long-term care, it can ease some of the burden for those specifically managing dementia care needs.

Medicaid

Medicaid does cover long-term care services, but eligibility depends on income and asset limits. Families may need to “spend down” savings to qualify. Rules vary by state, so it’s important to understand local requirements.

Private Pay Options

For many families, private pay strategies bridge the gap. These may include:

- Long-Term Care Insurance: Policies that cover certain types of care.

- Life Settlements: Selling an existing life insurance policy for cash.

- Reverse Mortgage: Using home equity to fund care expenses.

- Personal Savings & Investments: Out-of-pocket payments remain common.

Early planning can help reduce the financial burden, giving families more choices and flexibility.

The Bottom Line

Long-term care is something most families will face at some point, whether for an aging parent, spouse, or even themselves. By understanding the types of care available and knowing the true costs, you can make informed decisions that protect your loved one’s quality of life.

The key to long-term care planning is to start the conversation now. Planning ahead ensures that when the time comes, your loved one can receive the care they need without unnecessary stress or crisis decision-making.

If you’d like to explore non-medical home care as an option for your family, learn more about our in-home care services. Contact a local Caring office today.

anywhere")